The UCaaS/Hosted VoIP space has needed consolidation for years. Way too many providers, not enough buyers despite the TAM estimates that keep skyrocketing. Even in the midst of a pandemic, the move to cloud communications spiked but did not sustain. That means more consolidation especially with all the easy and cheap money floating around looking for returns on subscription revenue.

Skyswitch (a white-label provider utilizing Netsapiens softswitch) to BCM One. BCM One has also acquired WCS (a bandwidth reseller); Siptrunk.us; SIP.us; nexVortex (managed SIP operations); Arena One (Broadsoft based UCaaS provider in NY); and a partner of theirs, LincLogix, since February 2019. It gives them a BSFT UCaaS offering; a white label platform and a lot of managed SIP trunking.

Crexendo, a publicly traded UCaaS provider, purchased Netsapiens, a softswitch. This deal is still a mystery to me. BCM One and Axxess Networks should help Netsapiens grow users in the US.

Microsoft grabbed Metaswitch and is slowly bringing that to market in Azure Cloud and Operator. As MS Teams hits 250M monthly active users and 80M on Teams Phones monthly, Microsoft is winning. They also have a CPaaS platform, so they are just missing contact center.

AWS acquired Wickr, a secure collaboration tool used by the U.S Air Force. AWS offers Connect (CPaaS and CCaaS) and Chime (video). It seems that AWS is pushing into enterprise cloud comms with all the pieces – API, contact center, video, collab and voice. This will put them up against Twilio, Vonage, Microsoft and others. If AWS made it easy to add Amazon Payments, e-commerce and self-serve for businesses, they would hit $2T in revenue (yes trillion). Amazon reported Amazon Web Services (AWS) revenue of $13.5 billion for the QUARTER – Q1 2021, up 32%.

Sangoma buying Star2Star. S2S was looking for an exit; Sangoma is like a holding company for all things VoIP: Star2Star, VoIP Supply, e4, VoIP Innovations, Digium (Asterisk), Schmooze (FreePBX and PBXact), RockBochs (fax) and Micro Advantage (partner). This allows for offerings in CaaS, TaaS, UCaaS, MaaS, DaaS, FaaS, CPaaS and ACaaS according to Sangoma.

Vonage mixed all its offerings – CPaaS, CCaaS, UCaaS, VCaaS – into one bucket (VCS) two years ago. Then 8×8 did it earlier this year (calling it CXaaS, as if we need more acronymns that buyers don’t care about or understand!) This is just the showcase for the UC+CC era that buyers are examining. The highlight of that is Zoom acquiring Five9 for $14.7B last month to get some of the $26B cloud contact center business! [Spend $15B to get some of the $26B?!]

Broadvoice acquiring GoContact to add CCaaS to their UCaaS service offering (and get global reach since GoContact is in Europe) follows the UC+CC trend.

Dialpad buying Highrise and merging that plus UberConference into one app. (Their new name for it is TrUCaas according to Dialpad PR dept.)

So much activity that leaves many wondering about outcome – will they be able to integrate? What will the new offering look like/cost? How will they implement it? Will it work?

While all this integration is going on, the rest of the providers better grab some market share. Zoom and Microsoft (and to a lesser extent RingCentral) are taking all the air out of the room. It doesn’t leave much for the rest. I think that the top 20 providers will see 20%+ growth YoY but the rest of the group (#21 to #2001) will only see single digit growth. They just can’t compete with the branding, marketing, and sales strength of the top tier providers, who spent 10+ years putting it all together.

Additionally, there is the thinking: Do Buyers really want one vendor for all things? That is the thinking behind ecosystems & marketplaces, right? One stop shop for all your needs – like Aldi or Whole Foods, which in both cases is an example of one size does not fit all.

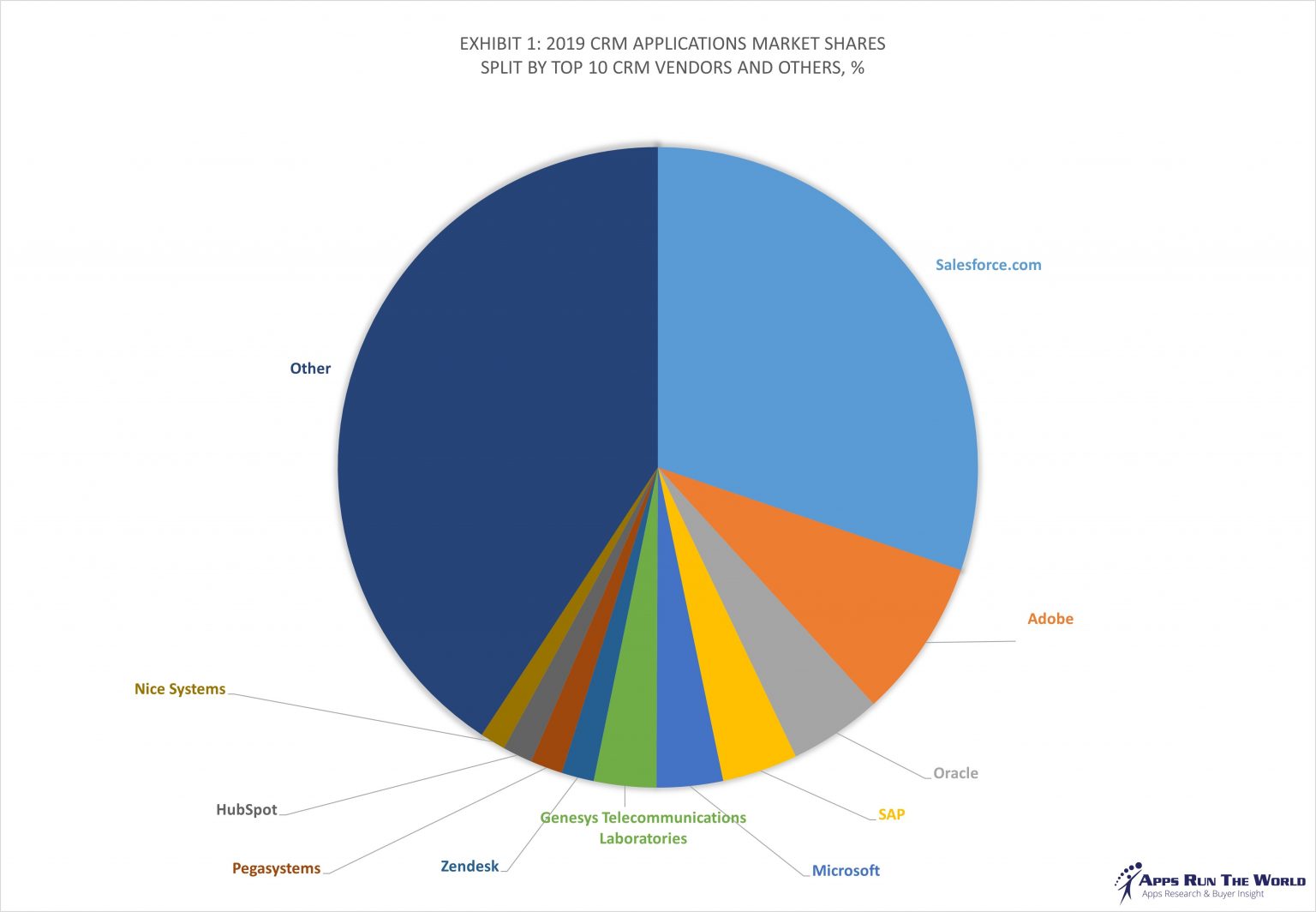

Enterprises in the past have purchased best of breed software, not an all in one. If they did, Microsoft would be the number one CRM (Dynamics 365) instead of fifth.

{kind=link}

The market is in flux, but then it is always in flux, except right now the rate of change is faster.

The things about consolidation: (1) synergies are harder to find in reality than on paper; (2) telecom integrations rarely come through; (3) fewer vendors hurt partners, distributors (decreased MDF) and buyers (less choice).